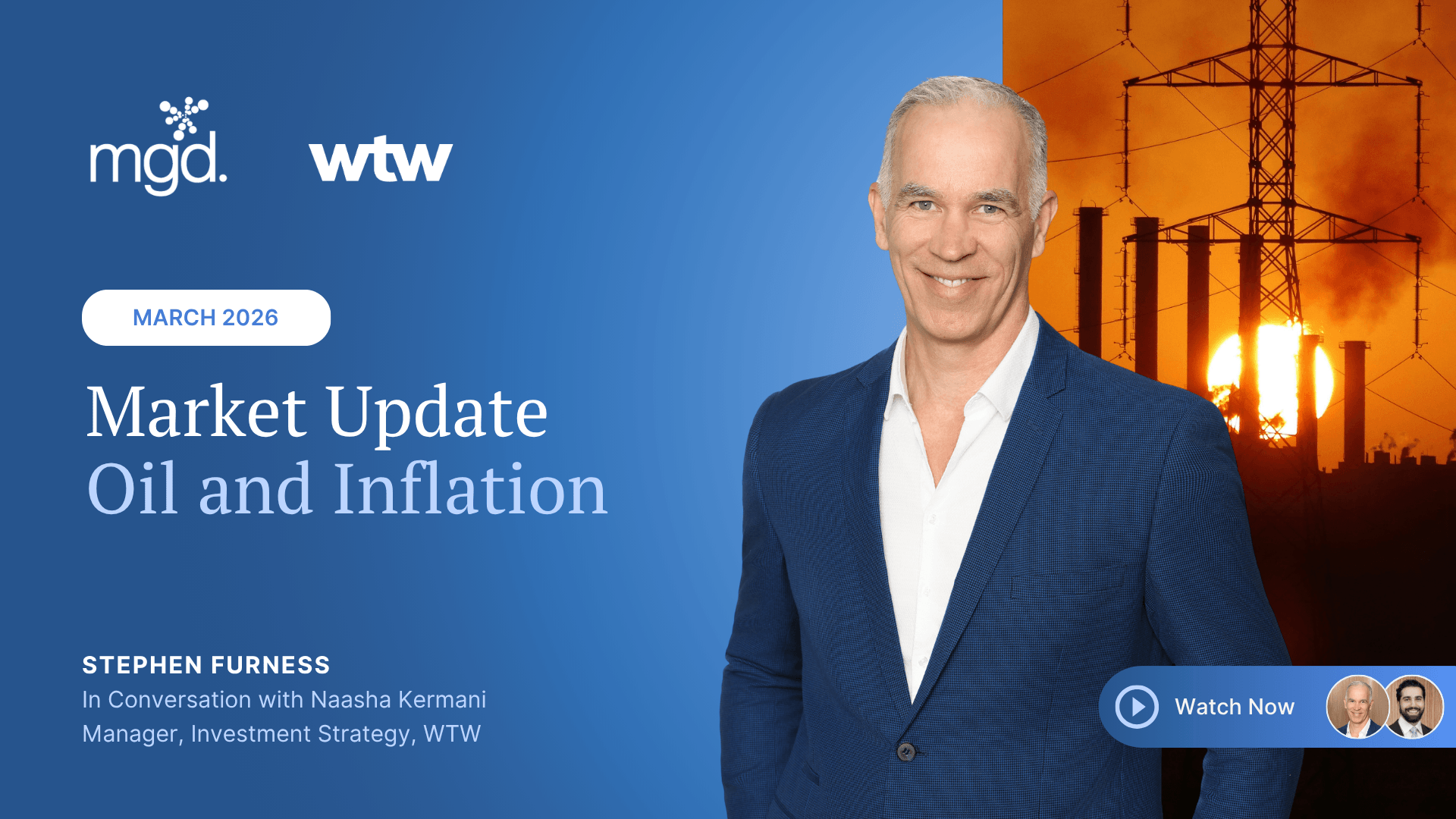

Market Update March 2026: Oil and Inflation

Recent geopolitical tensions have pushed oil back into focus, raising fresh questions for inflation, central bank policy and the path of markets from here.

In this March 2026 Market Update, Stephen Furness, Director and Investment Committee Chair at MGD Wealth, is joined by Naasha Kermani, Manager in the Investment Strategy team at WTW, to examine how the conflict involving Iran is flowing through to oil, inflation expectations and portfolio positioning.

Key Takeaways

The core outlook remains unchanged. WTW continues to expect that macro conditions by late 2026 and into 2027 will broadly align with earlier forecasts.

Inflation risks are conditional, not yet embedded. Oil-driven pressures are likely to prove transitory if the conflict is contained.

Australia’s inflation dynamics were already evolving. Domestic inflation pressures had already begun to re-emerge before the latest supply shock.

Equities retain near-term support. AI investment and fiscal expansion continue to underpin developed market earnings.

Market Conditions: Geopolitics Re-enters the Frame

The March 2026 backdrop has been defined by a sharp return of geopolitical risk. What had begun the year as a more conventional global investment outlook has been overtaken by renewed tensions in the Middle East, with markets quickly repricing oil, inflation risk and near-term uncertainty.

The key point, however, is that markets are not responding to geopolitics in the abstract. They are responding to the channels through which it may alter macro conditions—most obviously energy prices, inflation expectations and the policy path from here. WTW’s current assessment is that the conflict is likely to be relatively short-lived, even if the ride is uneven, and that the broader macro picture by late 2026 and into 2027 may still look broadly similar to where it stood at the beginning of the year.

Inflation and Oil: The Transmission Mechanism

Oil has become the clearest transmission channel between geopolitics and markets. As prices move higher, attention naturally turns to cost of living pressures, headline inflation and whether central banks may be forced to remain tighter for longer.

WTW’s baseline remains that, if the conflict subsides over the coming weeks, the inflationary impulse is likely to be transitory rather than self-reinforcing. Before the conflict, oil had already been moving lower as supply conditions improved. In that scenario, a ceasefire would allow oil prices to resume a softer trajectory over time, easing pressure on inflation and helping central banks continue their broader easing path.

Inflation and Policy: Why Duration Matters

The distinction now is less about whether inflation rises in the short term and more about whether it becomes embedded.

A brief supply shock is one thing. A more prolonged conflict is another. If higher oil prices begin to lift inflation expectations, feed into wages growth and create a reinforcing cycle across economies, the policy implications become more significant. That is not WTW’s central case at present, but it remains the key risk within the current market environment.

Australia: Pressure Was Already Building

For Australian investors, this matters because inflation was not entirely under control before the latest developments. Domestic inflation pressures had already begun to re-emerge in late 2025 and early 2026, driven less by oil and more by aggregate demand running ahead of the economy’s sustainable pace.

WTW described Australia’s growth “speed limit” as roughly 2 to 2.5 per cent. Once growth pushes beyond that range, inflationary pressures can begin to rebuild. That was already occurring before oil added another source of pressure. The Reserve Bank therefore enters this period with less flexibility than might otherwise have been the case

Equity Markets and the Longer-Term Outlook

Despite the increase in volatility, WTW has not materially changed its broader investment outlook. Its portfolio positioning for 2026 and early 2027 remains consistent with the views set out earlier in the year, on the basis that macro fundamentals are not expected to be materially different by the end of 2026.

That view continues to support developed market equities over the shorter term, helped by ongoing AI investment and robust fiscal expansion across major economies. Over a longer horizon, WTW also expects productivity gains from the AI cycle to contribute meaningfully to return drivers across portfolios

Portfolio Positioning: Diversification Still Matters

The longer-term capital market picture remains supportive of diversified, high-quality growth portfolios. International and Australian equities, along with other long-term return drivers such as property, debt, infrastructure and selective private market exposures, continue to play an important role within portfolio construction

That is consistent with the broader structure of MGD Wealth’s goals-based philosophy, where shorter-term spending needs are separated from long-term capital. In periods such as this, that structure becomes more valuable. It allows volatility to be absorbed where it belongs—within long-duration growth capital—without forcing near-term decisions around liquidity.

Risks: What Could Change the Picture?

The central question now is not whether markets remain volatile, but what would be required to alter the broader outlook.

For WTW, the answer lies in duration and transmission. A short-lived conflict that fades from oil markets would be one thing. A prolonged disruption that reshapes inflation expectations, lifts wage pressures and constrains central banks more meaningfully would be another. Until that line is crossed, the present environment appears more like a volatile interruption than a rewritten macro regime.

Positioning: A Bumpier Ride, Not Yet a Different Destination

The March 2026 update does not point to a wholesale change in direction. It points to a market environment that has become more fragile, more sensitive to energy prices and more attentive to inflation persistence.

That may well mean a bumpier path through the months ahead. But for now, the broader destination—slower disinflation, an eventual easing cycle, and continued support for diversified growth assets over time—remains broadly intact.

For any questions or to discuss your portfolio, reach out to your MGD Wealth advisory team.

Important Note: Stephen Furness is a Representative of MGD Wealth Ltd. AFSL 222600, ABN 53 009 079 725. Naasha Kermani is a Representative of Towers Watson Australia Pty Ltd AFSL 229921, ABN 45 002 415 349. The information in this article is current as of 23 March 2026. Please note that past performance is not an indication of future performance. Any advice included in this article is general and has been prepared without considering your objectives, financial situation or needs. As such, you should consider its appropriateness having regard to these factors before acting on it. Before you make any decision about whether to acquire a certain financial product, you should obtain and read the relevant product disclosure statement.